To generate $3,000 per month ($36,000 annually) in passive income, you typically need an investment portfolio between $450,000 and $1.2 million. The exact amount depends entirely on your portfolio’s annual yield or your chosen withdrawal rate. For example, a conservative 4% rule requires a $900,000 nest egg, while a more aggressive 8% yield reduces the required capital to $450,000.

However, chasing higher yields often comes with increased risk. At emerfd.co.uk, we advise investors to balance their need for monthly cash flow with the necessity of capital preservation to ensure the income lasts throughout retirement.

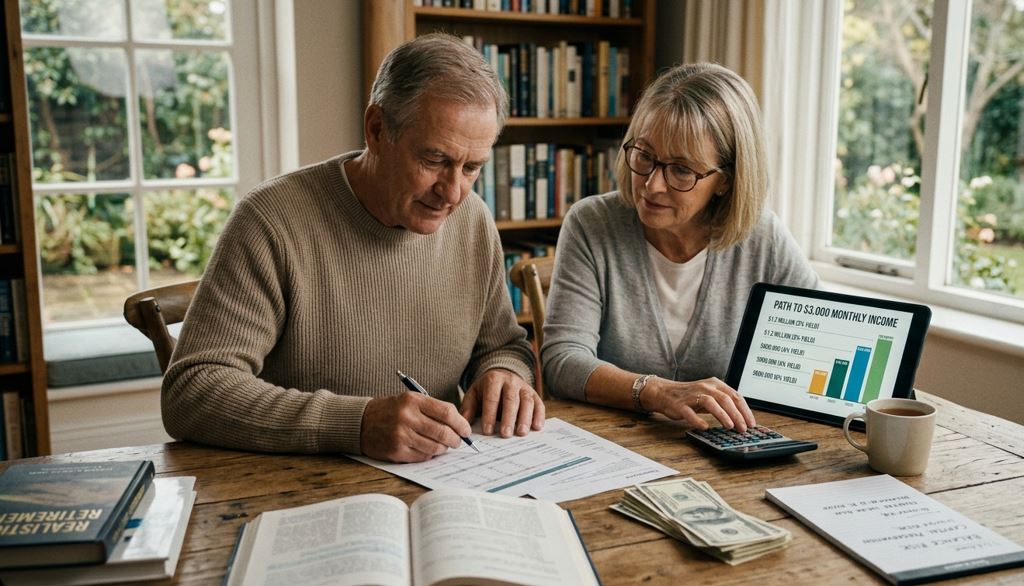

Capital Requirements Based on Annual Yield

The “magic number” for your financial independence depends on the return of your specific assets. Here is a breakdown of the capital required to hit a $3,000 monthly target:

-

3% Yield (Very Conservative): $1.2 Million. Typical for high-grade bonds or low-dividend growth stocks.

-

4% Yield (Standard): $900,000. Based on the “4% Rule” often used in traditional retirement planning.

-

6% Yield (Moderate): $600,000. Achievable through a mix of REITs, high-yield dividend stocks, or index funds.

-

8% – 10% Yield (Aggressive): $360,000 to $450,000. Requires specialized income-focused assets which may carry higher volatility.

Asset Classes for Generating Monthly Income

Investors typically use a combination of these vehicles to reach their monthly passive income goals:

-

Dividend-Paying Stocks: Companies that share profits with shareholders regularly.

-

Real Estate Investment Trusts (REITs): A way to earn rental income without managing physical property.

-

High-Yield Savings & CDs: Low-risk options that currently offer competitive rates for your liquid cash.

-

Annuities: Financial products that provide a guaranteed payout for a set period.

Factors That Impact Your Monthly Payout

You cannot simply look at the gross income; you must account for external factors that affect your spending power:

-

Taxes: Depending on your jurisdiction and account type (ISA, 401k, etc.), a portion of that $3,000 may go to the government.

-

Inflation: Over time, $3,000 will buy less. Your portfolio growth must ideally outpace inflation.

-

Market Volatility: If your principal drops significantly, maintaining a high withdrawal rate can deplete your funds prematurely.

Why Build Your Income Strategy with Emerfd?

While some platforms promise “get rich quick” schemes, Emerfd focuses on sustainable, long-term wealth creation. We provide the technical breakdowns and investment insights necessary to help you understand the true mechanics of compound interest and cash flow. Our goal is to move you from the saving phase to the living phase with total confidence.

Want to calculate your own path to financial freedom? Visit emerfd.co.uk today to explore our comprehensive guides on building a resilient and profitable investment portfolio.