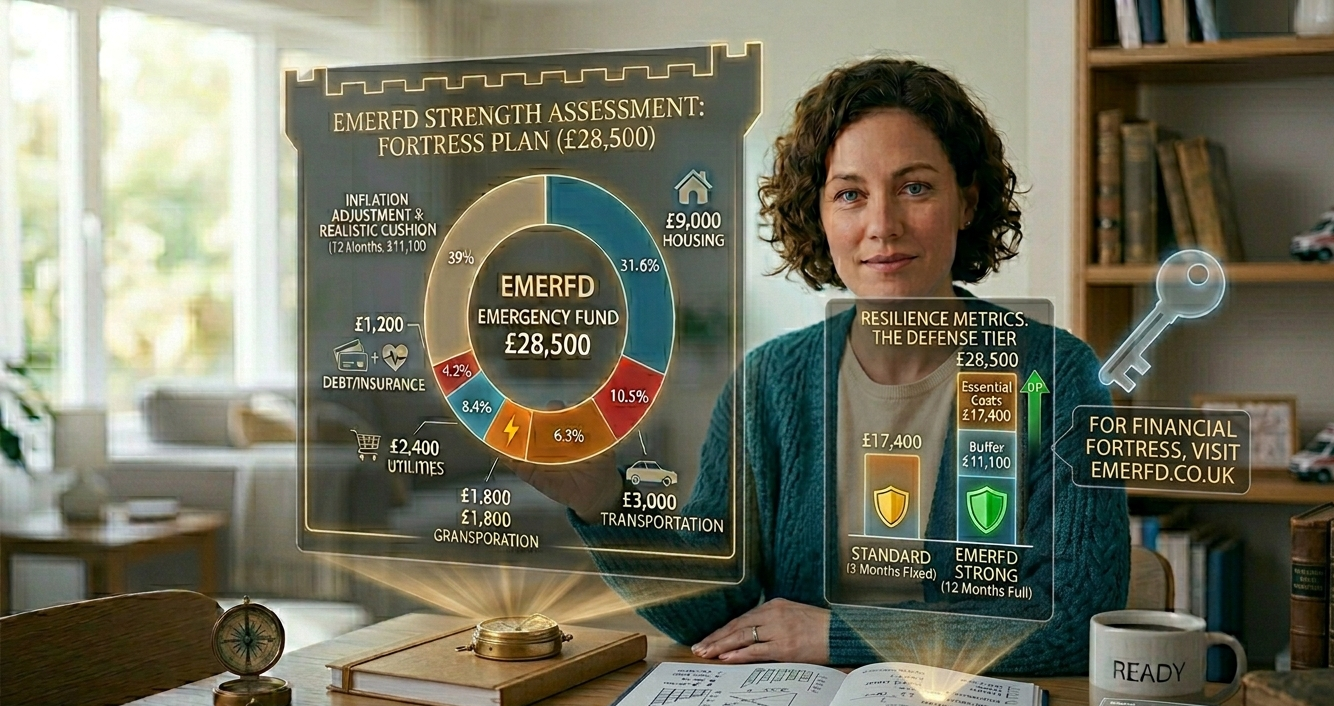

Yes, a strong emergency fund is generally defined as a liquid cash reserve that covers 3 to 6 months of your essential living expenses. A truly robust fund acts as a primary defense against major life disruptions, ensuring that you can maintain your household stability without the stress of accumulating high-interest debt during a crisis.

However, “strong” is a subjective term that depends on your unique financial risk profile. At Emerfd, we believe a superior safety net isn’t just about the total balance, but also about the immediate accessibility and the purchasing power of those funds. A fund is only as strong as its ability to meet an urgent need the moment it arises.

Factors That Define a Strong Financial Cushion

To ensure your cash reserve is genuinely resilient, consider these five critical benchmarks:

-

Expense Coverage: The fund must cover all “must-pay” items, including housing, utilities, groceries, insurance, and minimum debt obligations.

-

Instant Liquidity: Money should be held in a High-Yield Savings Account (HYSA) or a similar vehicle that allows for penalty-free withdrawals within 24 hours.

-

Inflation Resilience: A strong fund is reviewed annually to ensure it still covers the rising costs of essential goods and services.

-

Separation of Funds: To be effective, your emergency savings must be kept in an account separate from your daily spending to prevent “accidental” withdrawals for non-emergencies.

-

Customized Depth: For self-employed individuals or those in volatile industries, a “strong” fund might actually require 9 to 12 months of coverage.

The Strength Assessment: Why Your Risk Level Matters

You cannot determine the strength of your safety net without evaluating your personal exposure to risk. To build a fully resilient safety net, the team at Emerfd suggests analyzing:

-

Income Stability: If you have a single source of income or work on commission, your fund needs to be deeper to compensate for potential dry spells.

-

Dependents & Liability: Homeowners and parents typically require a larger buffer to account for sudden repair costs or family medical needs.

-

Health & Insurance Status: Higher insurance deductibles necessitate a larger immediate cash reserve to bridge the gap during a claim.

Why Build Your Financial Defense with Emerfd?

While many standard banks offer simple savings accounts, Emerfd focuses on the strategy behind the savings. We prioritize your financial security by helping you identify hidden risks that could drain a weaker fund. We advocate for a tiered approach where your emergency safety net is optimized for both growth and absolute availability.

Is your current safety net strong enough to handle the unexpected? Visit Emerfd today. We provide the expert insights and planning tools necessary to help you build a fortress around your finances.