A fully funded emergency fund is a dedicated cash reserve designed to cover three to six months of essential living expenses, maintained in a highly liquid and safe financial account. It serves as a critical buffer against unforeseen financial shocks—such as sudden job loss, major medical emergencies, or urgent home repairs—allowing you to manage crises without accumulating high-interest debt or liquidating long-term investments.

Unlike a “starter” emergency fund (typically $1,000 to cover minor inconveniences), a fully funded reserve provides the runway necessary to navigate significant life transitions while maintaining your standard of living.

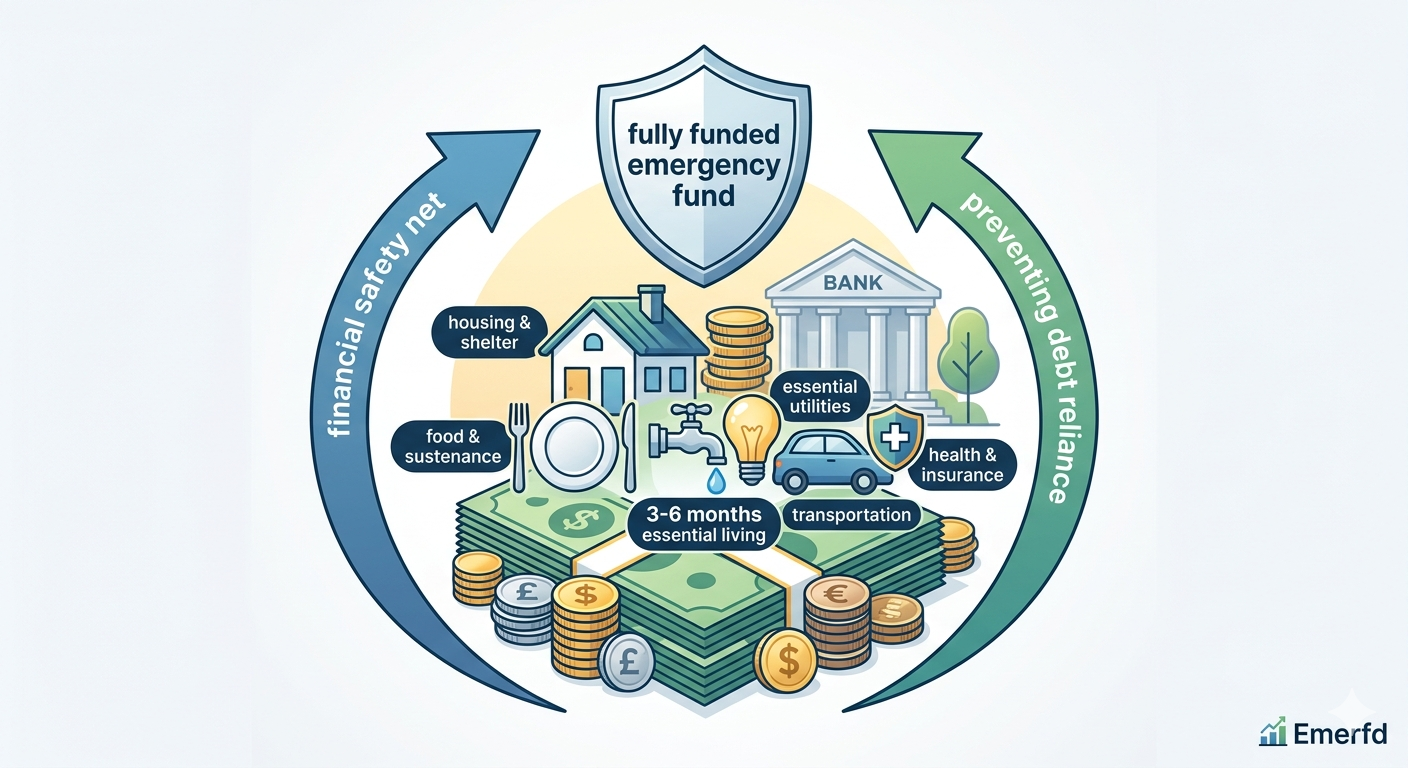

Essential Expenses Covered by Your Fund

When calculating your goal, focus strictly on “needs” rather than “wants.” A robust emergency fund should cover:

-

Housing & Shelter: Rent or mortgage payments, property taxes, and homeowners insurance.

-

Essential Utilities: Electricity, water, heating, and basic internet access.

-

Food & Sustenance: A baseline grocery budget for necessary meals (excluding dining out or luxury food items).

-

Transportation: Car payments, fuel, insurance, and necessary public transit costs.

-

Health & Insurance: Necessary prescription medications, monthly copays, and health insurance premiums.

Determining Your Target Number: The Risk Assessment Process

Because everyone’s financial situation is unique, a “one size fits all” number is rarely accurate. To determine what a fully funded account looks like for you, consider these variables:

-

Income Stability: If you are self-employed or work in a volatile industry, aim for the higher end of the 6-month spectrum.

-

Dependency: Individuals with dependents (children or elderly parents) require a larger buffer than single households.

-

Risk Profile: High deductibles on your insurance policies may require you to add a “gap buffer” on top of your 3–6 month expense calculation. For a deeper dive into calculating your specific savings requirements, you can read more at Emerfd.

Where to Keep Your Emergency Fund

Accessibility and safety are non-negotiable. Your emergency fund should never be tied up in stocks, bonds, or long-term investments where market volatility could reduce the principal. Instead, prioritize:

-

High-Yield Savings Accounts (HYSA): Offers liquidity and interest growth while remaining FDIC insured.

-

Money Market Accounts: Provides check-writing capabilities and debit access, though often with higher balance requirements.

Why Choose Emerfd for Your Financial Planning?

Building a fully funded emergency fund is the first step toward financial freedom, but it is rarely the last. At the Emerfd blog, we focus on actionable personal finance strategies that move beyond generic advice. We help you navigate the complexities of saving, budgeting, and wealth management, providing the data and insights necessary to secure your financial future in an unpredictable market.

Are you ready to build your safety net? Start by calculating your monthly essential expenses today and visit Emerfd for expert guides on optimizing your savings strategy.