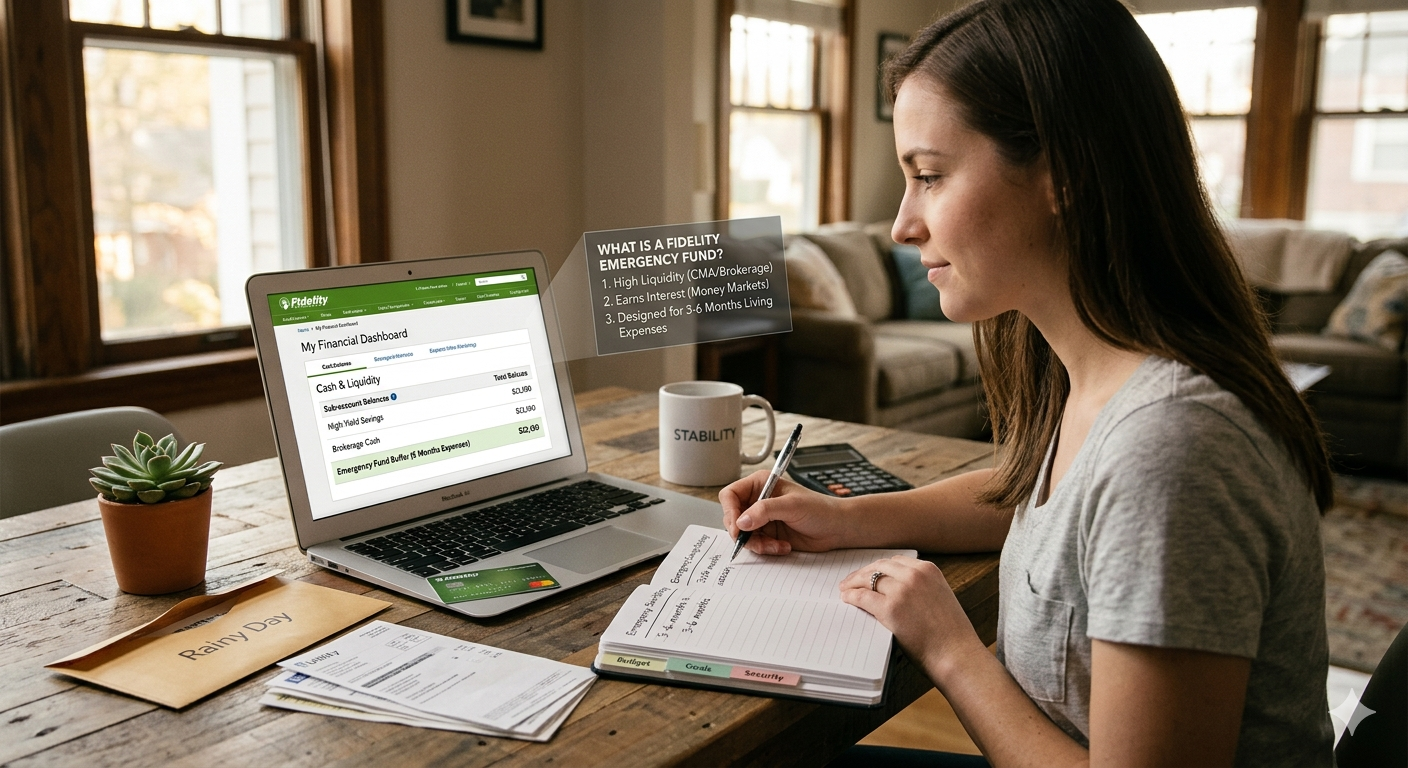

A Fidelity emergency fund is a dedicated savings strategy where individuals use Fidelity’s financial products—primarily the Cash Management Account (CMA) or a Brokerage Account—to house 3–6 months of living expenses. Unlike a traditional bank, a Fidelity emergency fund prioritizes a balance of immediate liquidity, capital preservation, and yield by automatically sweeping uninvested cash into high-interest money market funds like SPAXX.

Building an emergency savings buffer at Fidelity allows you to keep your “rainy day” money in the same ecosystem as your investments while keeping it separate from your daily spending.

Best Fidelity Accounts for Emergency Savings

Fidelity offers several vehicles that serve as an emergency fund repository, each with distinct advantages:

-

Cash Management Account (CMA): Acts like a high-yield checking account. It offers ATM fee reimbursements and no monthly fees, making it the most liquid option.

-

Brokerage Account: Best for those who want to manual-invest their fund into specific money market instruments or short-term CDs for higher yields.

-

Money Market Funds (e.g., SPAXX or FDLXX): These are the default “core positions” where your cash sits, earning interest rates that often significantly outperform traditional savings accounts.

Why Use Fidelity for Your Emergency Fund?

While many banks offer savings accounts, a Fidelity liquid reserve provides unique features for financial security:

-

Auto-Liquidation: If you spend money via a debit card or check, Fidelity can automatically sell your money market shares to cover the transaction.

-

Competitive Yields: Your cash earns a market-based rate of interest without being “locked away” like a traditional CD.

-

No Minimums: You can start your financial safety net with as little as $1, making it accessible for everyone.

The Planning Process: How Much Do You Need?

To ensure your emergency fund is effective, financial experts recommend a specific evaluation process:

-

Calculate Essential Expenses: Focus on housing, utilities, groceries, and insurance—not discretionary spending.

-

Assess Job Stability: If you are a freelancer or in a volatile industry, aim for 6–12 months of coverage.

-

Determine Your Core Position: Choose a core fund that matches your tax situation (e.g., municipal money markets if you are in a high-tax bracket).

Why Choose an Organized Strategy for Your Treatment?

Relying on a standard savings account often means losing value to inflation. By utilizing a structured Fidelity cash strategy, you prioritize both safety and growth. This ensures that when an unexpected medical bill or car repair arises, your money is not only available but has been working for you in the meantime.

Ready to secure your financial future? Explore our guides at Emerfd to learn how to optimize your liquidity and savings today.